Back to Blog

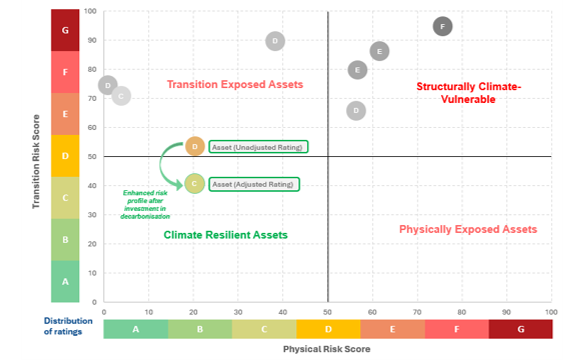

Constructing an on-site carbon capture facility moved this asset from a ‘D’ to a ‘C’ Climate Risk Rating, improving its projected climate-induced net value loss by 2050 from −13% to −7% relative to its peers.

Figure: Risk profile of our client’s referenced energy and heat generation asset, before and after decarbonisation measures, shown against comparable assets in the same TICCS class.

What is the benefit of action versus the cost of inaction?

Key takeaways

Infrastructure assets face material physical and transition climate risks that can erode cash flows and value, but targeted decarbonisation can measurably improve an individual asset’s risk profile.

- The Climate Risk Rating (CRR) translates that risk into a forward-looking financial view of how climate change may affect performance, cash flow, and valuation, incorporating mitigation where applicable.

- Mitigation requires upfront capital, but it lowers future carbon costs, reduces regulatory exposure, and strengthens resilience.

- The CRR lets asset owners quantify the benefit of action against the cost of inaction, and an improved rating is a value-creation lever across the holding period and at exit.

The exposure

Scientific Climate Ratings worked with a client in the heating and energy generation sector. On a business-as-usual path, the asset’s carbon footprint would have driven a significant and rising carbon cost, the product of its Scope 1 and 2 CO₂-equivalent emissions and the country’s carbon tax ($ per tonne CO₂). The sector had already absorbed a 200% rise in carbon tax in the two years before the project, with further increases projected, pushing high-emitting assets toward becoming ‘stranded’.

Stranded assets: assets forced to cease operations before their natural end owing to prohibitive transition risks.

The decarbonisation investment

The client is constructing an on-site carbon capture facility to mitigate its operational emissions and the associated carbon tax, achieving close to a 90% reduction in emissions versus business-as-usual over 10 years. The project received state support, aligning with the country’s net-zero ambitions.

The quantified financial impact

As a result, the asset’s CRR improved from ‘D’ to ‘C’, shifting from ‘transition-exposed’ to ‘climate-resilient’. Its projected climate-induced net value loss by 2050 narrowed from −13% (without mitigation) to −7% (with the decarbonisation measure factored in).

More information on an asset’s climate risk vulnerability: Given that infrastructure assets are largely immobile, operate over long timeframes, and encompass many high-emitting activities, they are inherently vulnerable to climate-related operational disruptions and financial losses. The extent of an asset’s climate risk vulnerability can be categorised in four buckets:

-

- Transition-exposed: an asset that faces high transition risk owing to the carbon costs of undertaking high-emission activities in a low-carbon economy.

- Physically exposed: an asset that faces high physical risk from vulnerability to extreme weather events and higher average temperatures.

- Structurally climate-vulnerable: an asset that faces physical and transition risk and thus requires both resilience and decarbonisation measures.

- Climate-resilient asset: an asset with a low exposure to physical and transition risks.

Vulnerability (to physical risks): the propensity or predisposition of an asset to be adversely affected by a hazard event.

The value for investors

Quantifying physical and transition impacts in financial terms lets investors and asset owners decide where to allocate capital and which measures offer the greatest return. This protects future cash flows and can enhance value where an asset becomes relatively low-risk against its peers, supporting stronger long-term earnings, greater investor demand, and stable valuations through to exit.